Overview

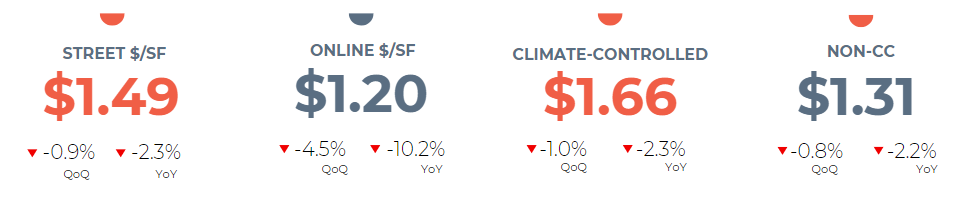

The self-storage market in 3Q 2024 reflected an industry-navigating transition, pressured by elevated interest rates, inflation, and regional oversupply. Average street rates declined 0.9% quarter-over-quarter and 2.3% year-over-year to $1.49/sq ft., while promotional rates dropped more steeply by 10.2% year-over-year to $1.20/sq ft., signalling heightened competition and increased reliance on discounts to maintain occupancy.

This competitive pressure stems from oversaturation, driven by a surge in pandemic-era development that left many new facilities struggling to stabilize in overbuilt markets. Despite these challenges, demand for climate-controlled units and premium features remains strong, particularly in Sun Belt states like Florida, North Carolina, and Georgia. Shifting housing dynamics further bolster demand, with renter households – growing three times faster than homeowner households and now comprising over 35% of U.S. households – driving the need for flexible, affordable storage solutions.

REITs also played a pivotal role in shaping the market during the quarter, driving consolidation and operational modernization through acquisitions, development, and third-party management expansion. Their efforts have elevated competition, set higher standards, and showcased the sector’s adaptability to changing economic conditions.

REIT Performance and Market Impact

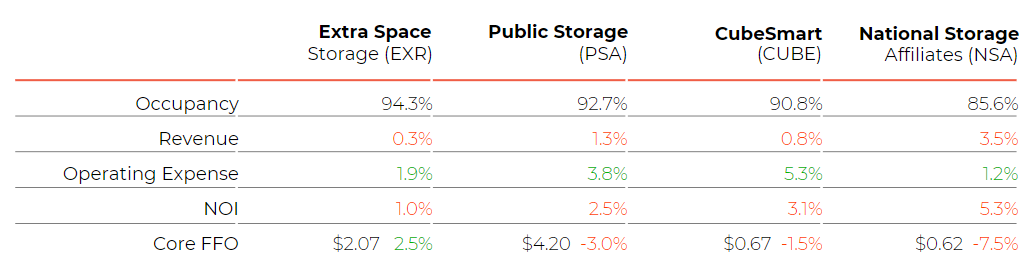

Self-storage REITs delivered mixed results in 3Q 2024, demonstrating their ability to navigate economic pressures and evolving market dynamics. Strong occupancy levels offset moderate year- over-year revenue declines, reflecting steady tenant demand. However, operating expenses rose 1-5% during the same period, driven by higher property taxes, increased marketing costs, and severe weather impacts like Hurricane Milton, which cost Extra Space Storage over $10 million. Integration challenges also played a role, including a $51 million impairment loss related to Extra Space’s merger with Life Storage. Despite these headwinds, REITs remained focused on growth during the quarter, amplifying competition in key self-storage markets.

During the quarter, REITs expanded their presence, each pursuing a distinct growth strategy. Extra Space grew through acquisitions and the expansion of its management platform. The company invested $163.9 million to acquire ten stores and one Certificate of Occupancy and added 63 stores to its management platform, increasing its total to 1,921 properties under management. Additionally, Extra Space contributed $30.7 million to a joint venture. In contrast, Public Storage allocated $23.3 million to acquire three facilities and committed over $1 billion to new development projects.

Amid rising costs and intensifying competition, REITs capitalized on their scale, operational efficiencies, and consolidation strategies to adapt to challenges. These efforts continue to position the sector for long-term growth and stability in an increasingly competitive landscape.

In 3Q 2024, average street rates for self-storage stood at $1.49/sqft., down 0.9% quarter-over-quarter and 2.3% year-over-year, while online promotional rates ended the period at $1.20/sqft., reflecting steeper declines of 4.5% over the quarter and 10.2% compared to last year. Climate-controlled units maintained their premium, averaging $1.66/ sqft., compared to $1.31/sqft. for non-climate-controlled units, though both categories experienced similar year- over-year declines of approximately 2.3%.

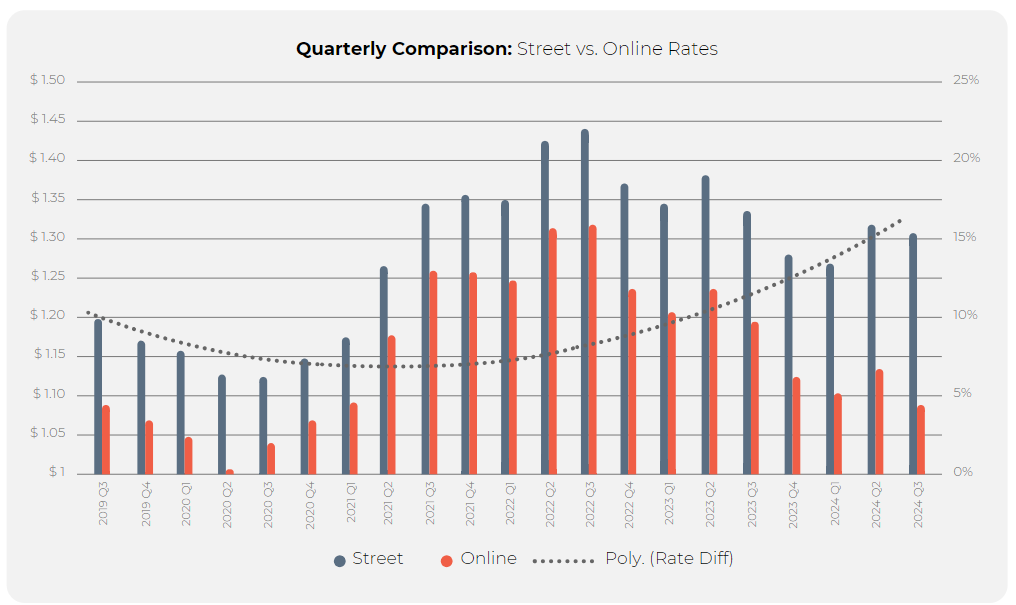

From 2019 through 2024, self-storage rates have mirrored the economic and market volatility of the times. The spread between street and online promotional rates fluctuated significantly, from a low of 6.6% in Q3 2021 when demand was robust and operators maintained strong pricing power to a record-high 20.2% in Q3 2024. This widening gap reflects the growing reliance on aggressive promotional strategies as demand softened over the past year amid economic uncertainties.

Market Drivers Behind the Gap

The increasing rate differential reveals operators’ strategies to attract price-sensitive, short-term renters in a more competitive environment. Declining online rates signal intensified efforts to fill vacancies as oversupply and slowing demand exert downward pressure on occupancy. These promotions often come at the expense of long-term revenue per square foot, as discounts erode profitability while driving higher tenant turnover.

Interestingly, the persistence of premium pricing for climate-controlled units suggests a continued willingness among tenants to pay for features that protect valuable items, even as broader economic pressures influence decision-making. This highlights the duality of the market: while price sensitivity grows, a segment of renters prioritizes quality and convenience, keeping demand for premium options relatively stable. Download the entire report.

Implications for the Industry

The record-high 20% rate spread underscores shifting tenant preferences and the growing reliance on promotions to sustain occupancy in today’s competitive market. While effective as a short-term tactic, overusing discounts risks undermining long-term revenue potential and property valuations, particularly when demand stabilizes. This dynamic highlights the need for strategic pricing models that balance competitive rates with initiatives to maintain tenant loyalty and offer premium features. For operators, the widening gap is both a challenge and an opportunity to refine acquisition and retention strategies, ensuring adaptability in an evolving economic landscape.

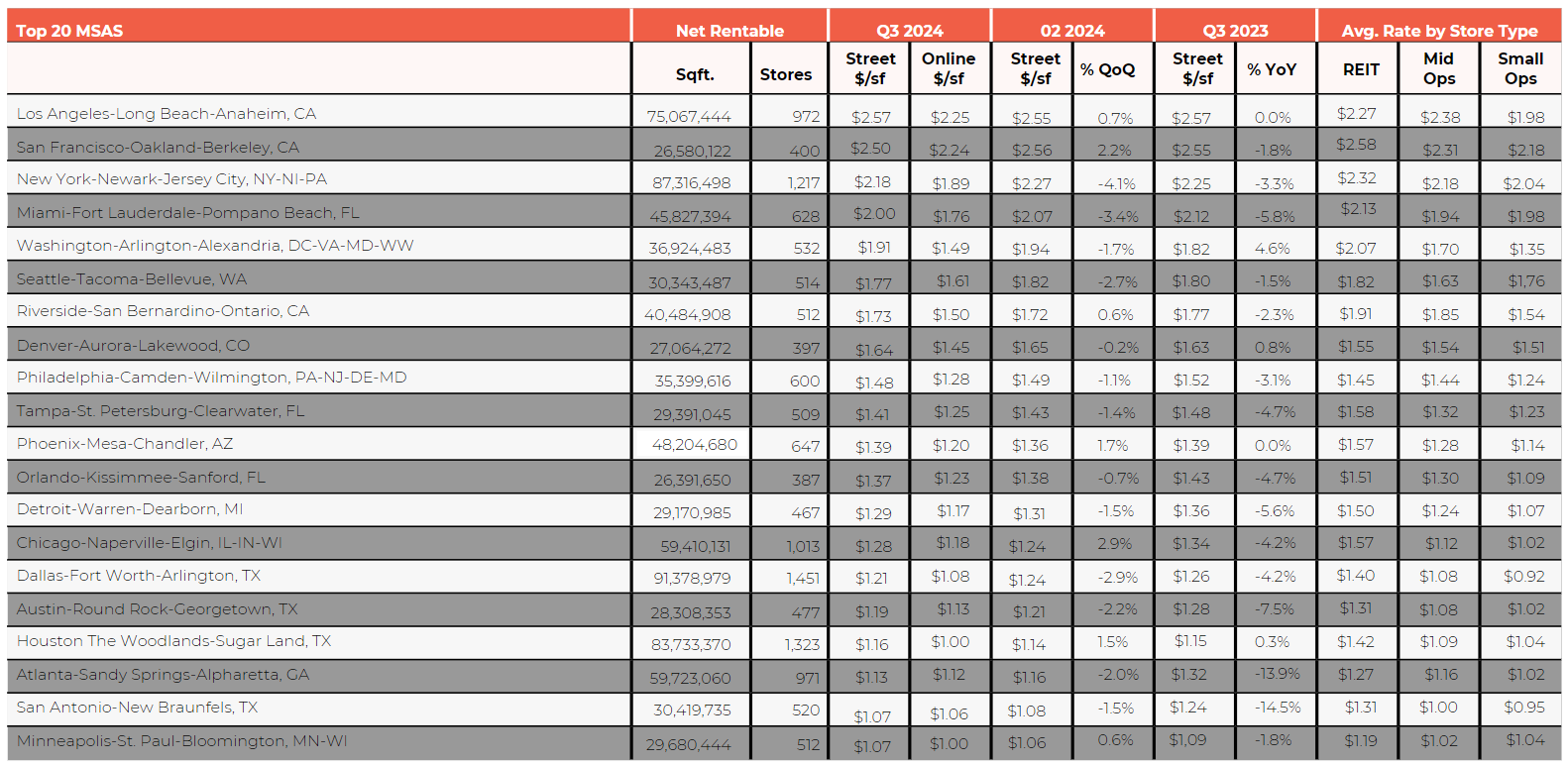

The Top 20 self-storage MSAs accounted for approximately 30% of the U.S.’s total inventory of over 2.8 billion net rentable square feet, with Texas leading as a major contributor, hosting nearly 10% of the national inventory across its Dallas, Houston, and San Antonio MSAs. Among these markets, REIT-owned facilities dominate, controlling 40-50% of net rentable stock in the largest MSAs, underscoring the institutional influence on market dynamics.

Rate Dynamics in Major MSAs

Urban MSAs faced negative rent growth over the past year but showed signs of recovery in the third quarter. However, economic pressures and oversupply continue to challenge market performance. For instance, self-storage operators in larger MSAs prioritized maintaining occupancy over revenue growth, as reflected in the widening gap between street and online promotional rates. Markets like Washington, D.C. and Los Angeles recorded spreads of $0.42 and $0.30 per square foot, respectively, indicating substantial reliance on discounts to keep their units filled. In markets like New York and Miami, rates declined over 3% during the quarter, highlighting the ongoing challenge of balancing occupancy and revenue. This growing dependence on promotions could strain long-term revenue per square foot, particularly in oversupplied regions like Atlanta and San Antonio, which experienced the most significant declines of approximately -14% year-over-year.

Premium markets such as San Francisco and Los Angeles, averaging over $2.50/sqft., continued to demonstrate pricing power due to their enduring appeal as cultural and economic hubs. However, even these regions faced challenges from inflation and reduced consumer spending, which have dampened pricing flexibility. Conversely, markets like Chicago and Phoenix demonstrated resilience with modest quarter-over-quarter growth (3% and 1.5%, respectively), signaling improving tenant demand.

Demographics and Demand Drivers

The demand for self-storage in large cities is driven by demographic trends and economic factors. Cities like New York, Los Angeles, and San Francisco continue to attract young professionals and families with job opportunities, cultural amenities, and strong infrastructure, despite high housing costs. This steady demand is further supported by a rebound in urban populations following the pandemic, with recent Census Bureau data showing many large cities saw reduced losses or population gains from July 2021 to July 2022. Urban centers remain key hubs for jobs, social networks, and amenities, driving the need for storage solutions in smaller living spaces.

The self-storage sector is poised for a rebound in 2025, driven by easing interest rates, increased transaction activity, and steady demand tied to housing trends. Rising operating costs are encouraging operators to adopt tech-driven efficiencies to optimize pricing, identify profitable submarkets, and manage expenses. While oversupply in certain regions remains a challenge, the sector’s resilience and adaptability support its long-term growth potential.

Experts predict a period of normalization, with stabilized occupancy levels, moderate rental rate increases, and growing institutional interest as capital continues to seek opportunities in the space. Improving lending conditions and a resurgence in residential real estate activity could further fuel demand for storage solutions in the coming year.

Though market saturation may temper the outsized returns seen in previous decades, self-storage remains a reliable asset class with steady performance potential, supported by its consistent demand and ability to navigate changing market conditions.

- Declining Rates: Street rates fell 0.9% quarter-over- quarter and 2.3% year-over-year to $1.49/sqft., while promotional rates dropped 10.2% year-over-year to $1.20/ sqft., reflecting increased competition and reliance on discounts

- Oversupply Challenges: Pandemic-era overbuilding has driven oversaturation in some markets, pressuring rents and making stabilization difficult for new facilities

- REIT Influence: REITs shaped pricing dynamics by using aggressive promotional strategies to maintain occupancy while investing heavily in premium features like climate-controlled units. This drove competitive pressures in oversupplied markets while sustaining higher pricing in urban areas with constrained supply

- Widening Rate Gap: The record-high 20.2% spread between street and promotional rates highlights growing reliance on discounts to attract tenants, raising concerns about long-term revenue potential

- Demographics Fuel Growth: Renter households, now 35% of U.S. households, are growing three times faster than homeowner households, sustaining demand for flexible storage solutions