Self-storage buyers always ask about CAP rates. First, a capitalization (“CAP”) rate in principle is quite a simple calculation – take the Net Operating Income (NOI or EBITDA) and divide it by the asking price and the resulting number is the CAP rate. This represents the return an investor would expect over a one-year period. In some cases, it is the expected first-year income, in other cases it is the most recent (aka trailing 12-month) annual net operating income.

Capitalization Rate = Net Operating Income / Current Market Value (or asking price)

Sounds simple. What’s not to love about a CAP rate! The issue in the self-storage industry is that the basis for gross income and total expenses isn’t quite as clear-cut as it may be with a NNN leased investment property where the rent is known, and the expenses are passed through to the tenant(s). In self-storage, there is no certainty in what gross income will be for the next twelve-month period. With the short-term nature of leases and dynamic pricing models, rents can fluctuate quite a bit. Looking at the most recent twelve-month gross income numbers is the easiest way to determine the gross income number, however, in most cases, this leaves money on the table and doesn’t give credit for potential improvements in income (rent increases, addition of tenant protection income, etc.). Buyers today will generally underwrite the CAP rate based on the most recent twelve months’ gross income numbers.

On the expense side, the math can get fuzzier. If a property is professionally managed by a 3rd party the reports can be relatively clean and require only minimal adjustments. One expense to keep an eye out for is property taxes, in many cases this is paid by the owner, not the manager and will need to be added back and then adjusted based on a post-sale reassessment.

If a property is owner managed there are any number of adjustments that may be required. These could include:

- Owner’s vehicle expenses

- Personal or family cell phone bills

- Owner payroll or distributions

- 3rd party management fee

- Payroll (could go up or down, adjusted to “as typical”)

- Advertising

- Property taxes

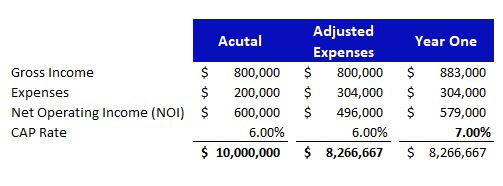

Above is a typical scenario for an owner managed property with below market expenses, in this case at 25%. After as-typical adjustments expenses are 38%. A seller’s expectation of value at a 6% CAP rate may be $10,000,000, but a realistic price after adjustments would be closer to $8.3 million. Assuming an acquisition at that number, implementing aggressive in-place rate increases (ECRI), adding tenant protection and increasing administrative and late fees could push your first-year return to closer to a 7% return.

Above is a typical scenario for an owner managed property with below market expenses, in this case at 25%. After as-typical adjustments expenses are 38%. A seller’s expectation of value at a 6% CAP rate may be $10,000,000, but a realistic price after adjustments would be closer to $8.3 million. Assuming an acquisition at that number, implementing aggressive in-place rate increases (ECRI), adding tenant protection and increasing administrative and late fees could push your first-year return to closer to a 7% return.

This is very typical of transactions we are seeing in the market today. In 2021-2022 buyers were paying for this additional upside by offering somewhere between the $8.5 and $10.0 number (perhaps a 5.0% – 5.5% CAP rate equivalent) with the SELLER’s receiving much of the credit for any upside. In today’s higher interest rate, more challenging, market deals are transacting based on adjusted income numbers with the BUYER’s receiving the benefit of any upside.

The difference between the $8.3 and $10.0 figure is the bid-ask spread and one reason transaction volumes are down. To achieve a stable, normalized market we will need to see seller capitulation to the current market.

About the Author:

Tom de Jong is an Executive Vice President with Colliers International and a founding member of the “de Jong I Becher Self Storage Team” one of the top brokerage teams in the self-storage industry within the US.