Anyone following the self-storage industry over the past decade has seen the impacts of institutional capital (private equity, HNW family offices, hedge funds, endowments, etc.). Primary impacts include:

The rise of REIT 3rd party management platforms

- Institutional capital generally mandates institutional property management. The self-storage REITs, primarily Extra Space, CubeSmart, Public Storage, and now SmartStop, have been the main beneficiaries of this shift in the capital stack. Prior to the entrance of institutional capital, the REITs’ growth came from development and acquisition activity that has now shifted to adding properties to their platforms through their management platforms. Secondary beneficiaries have been the privately held national and regional players, including StorageMart, Prime Storage, Storage Asset Management (SAM), US Storage Centers (Westport), Storage King USA (Andover), and others.

Development accelerated

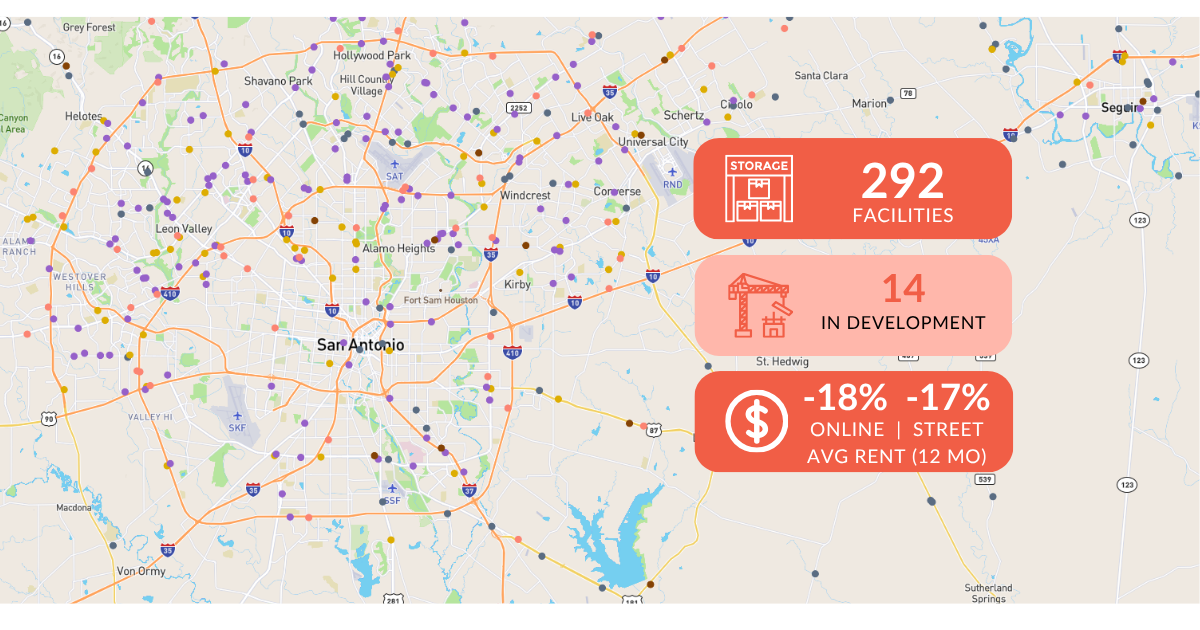

- The amount of new supply and the type of construction changed materially with the addition of institutional money. Every market across the country has experienced a significant increase in newly developed assets, with most of these assets being multi-story, climate-controlled facilities, a major shift from the 100% drive-up facilities from the 1980 and 1990’s.

CAP rates compressed

- Once the capital has been allocated to a property sector, it generally is use-it or lose-it money. This places extra pressure on finding deals for acquisitions or development. More money chasing deals inherently pushes up prices, compressing CAP rates and pushing out individual, smaller investors.

Industry consolidation

- The self-storage industry has been going through a rapid consolidation. As the industry has matured and the money has poured in we have seen the rise of billion dollar ++ capital commitments. This has led to an inevitable consolidation within the space that shows no end in sight.

The thing about private equity and most other institutional sources of capital is that there is an expiration date, based on the initial investment thesis presented to their capital sources. Typical fund timelines call for a 5-to-7year life cycle from the day the funds are provided to the day the assets are sold – aka the Exit Date. The way these projects were initially financed was designed to match their thesis. The high-water mark of capital entering the space was in 2021, now five years ago, leading to the natural end of the life cycle for many. Challenges in the economics of the self-storage sector have been well documented – higher-for-longer interest rates, a challenging rental rate market, declining occupancy levels, increasing expenses all leading to dropping net operating incomes (NOI) and declining asset values.

All of this leading to many self-storage market participants asking “Where’s the Exit”?

About the author: Tom de Jong is an Executive Vice President with Colliers International and a founding member of the “de Jong Self Storage Team I COLLIERS” one of the top brokerage teams in the self-storage industry. To discuss this article or to find out what your assets are worth today connect with Tom de Jong.